First-time homebuyer grants provide thousands of dollars in free financial assistance to help cover down payments, closing costs, and other homeownership expenses. Offered by federal, state, local, employer, and nonprofit programs, these grants are often overlooked despite broad eligibility. Understanding how they work can significantly reduce the cost of buying your first home and accelerate homeownership.

For millions of Americans, buying a first home feels like a distant dream. Rising home prices, high interest rates, and the belief that a massive down payment is required keep many people renting far longer than they want to.

What most first-time buyers are never told is that there is real, legitimate free money available to help them buy a home—money that doesn’t need to be repaid.

Every year, billions of dollars in first-time homebuyer grants go unused across the United States. Not because people don’t qualify—but because they don’t know these programs exist.

Take Emily and Ryan, a newly married couple in Ohio. They postponed buying because they believed they needed at least $40,000 saved. After meeting with a housing counselor, they learned they qualified for a state grant and a city-level program that covered their down payment and most closing costs. They bought their home with less than $3,000 out of pocket.

Their story isn’t rare. It’s typical.

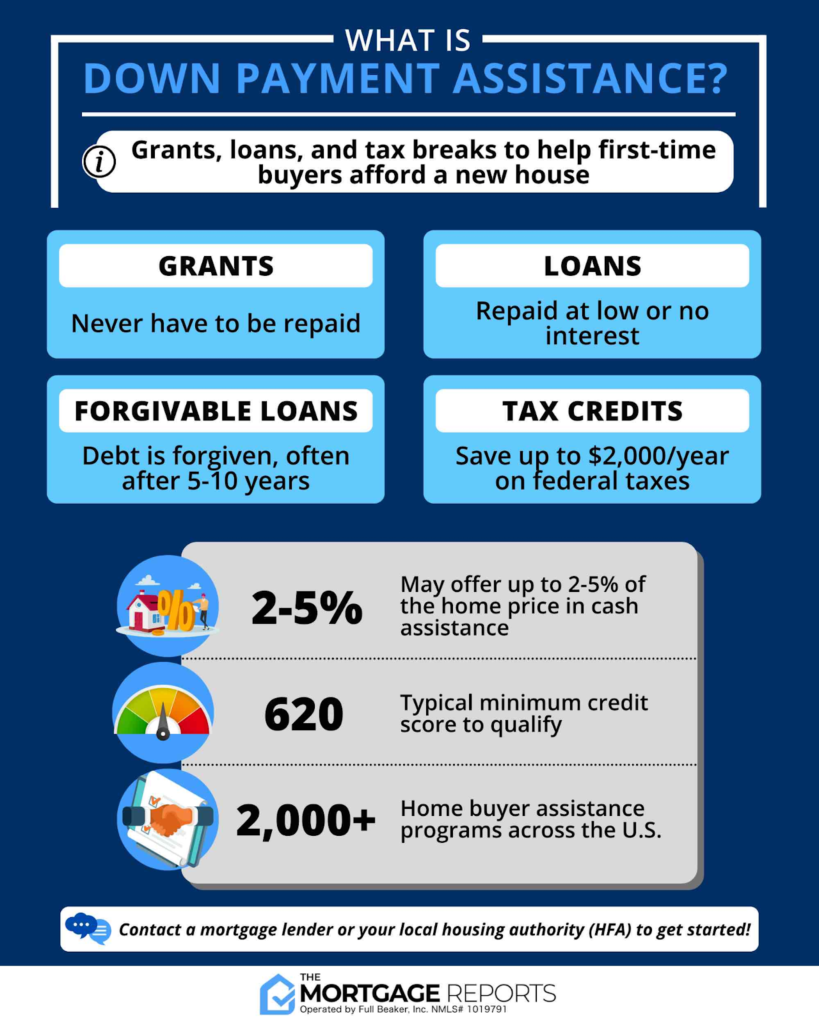

First-time homebuyer grants are financial assistance programs that provide free money to eligible buyers to reduce the upfront cost of purchasing a home.

Unlike loans:

- Grants usually do not require repayment

- They do not increase monthly mortgage payments

- Many are forgiven immediately or after a short occupancy period

These programs exist to:

- Increase homeownership rates

- Stabilize neighborhoods

- Support working families

- Strengthen local economies

- Down payment assistance

- Closing costs

- Interest rate reductions

- Mortgage insurance premiums

- Required homebuyer education fees

For many buyers, grants reduce upfront costs by $5,000 to $25,000 or more, dramatically lowering the barrier to homeownership.

One of the biggest misconceptions is that “first-time” means never owning a home before. In reality, most programs define a first-time buyer as someone who has not owned a primary residence in the last three years.

You may qualify if:

- You’ve been renting for the last 3+ years

- You sold a home years ago

- You’re divorced and no longer on a mortgage

- You previously owned property with an ex-spouse

Marcus, a 38-year-old logistics manager, assumed he was ineligible because he owned a home a decade ago. After renting for several years, he discovered he qualified again and received $10,000 in assistance.

The amount varies based on location, income, and program structure, but the numbers often surprise buyers.

Typical assistance amounts include:

- $5,000–$10,000 from state housing programs

- Up to $25,000 in high-cost or revitalization areas

- Additional assistance from city or nonprofit programs

Many buyers are able to stack multiple grants, combining:

- State programs

- City or county assistance

- Employer-sponsored housing benefits

- Nonprofit grants

This strategy can reduce out-of-pocket costs to nearly zero.

Federal housing initiatives often serve as the foundation for grant programs nationwide. While federal grants are usually administered locally, they play a critical role in affordability.

These programs typically support:

- Low-to-moderate income households

- Rural homebuyers

- Veterans and public servants

- Underserved communities

They often work alongside state and local grants rather than replacing them.

Every U.S. state offers some form of homebuyer assistance, yet many residents never hear about it.

State programs often:

- Offer $7,500–$15,000 in assistance

- Focus on first-time and moderate-income buyers

- Require a short homebuyer education course

In California, eligible buyers can access shared appreciation or forgivable assistance programs that significantly reduce upfront costs.

Local grants are often the most generous—and least publicized.

Cities use these programs to:

- Encourage owner-occupied housing

- Revitalize neighborhoods

- Stabilize property values

Local programs may cover:

- 100% of closing costs

- Down payment grants

- Emergency repair reserves

Because funding is limited, these programs are often first-come, first-served.

A growing number of employers quietly offer housing assistance as part of employee benefit packages.

Industries commonly offering grants include:

- Healthcare

- Education

- Government

- Technology

- Public safety

Employer benefits may include:

- $5,000–$20,000 in forgivable assistance

- Matching down payment programs

- Preferred mortgage partnerships

Many employees never realize these benefits exist.

Nonprofit organizations play a crucial role in expanding access to homeownership.

They often focus on:

- First-generation buyers

- Teachers, nurses, and essential workers

- Minority and underserved communities

Nonprofit grants are frequently layered with government programs, increasing total assistance.

A common myth is that grants are only for very low-income households.

In reality:

- Many programs allow incomes up to 120–140% of area median income

- Dual-income households often qualify

- High-cost areas have higher income caps

In some metro areas, households earning $150,000+ annually may still qualify.

Another major misconception is that grants require excellent credit.

In practice:

- Many programs accept scores as low as 620

- Some allow alternative credit histories

- Counseling programs help buyers improve eligibility

Consistency and financial readiness matter far more than perfection.

While each program is different, the process typically includes:

- Mortgage pre-approval with an approved lender

- Completion of a HUD-approved homebuyer education course

- Income and asset documentation

- Property eligibility review

- Grant approval at or before closing

Most buyers report the process is far less intimidating than expected once they begin.

Even qualified buyers sometimes lose eligibility due to avoidable errors:

- Working with non-approved lenders

- Applying after funds are depleted

- Assuming ineligibility without checking

- Skipping required education courses

- Purchasing before grant approval

The biggest mistake of all is waiting too long.

Reliable sources include:

- State housing finance agency websites

- HUD-approved housing counselors

- City and county housing departments

- Approved mortgage lenders

- Employer HR benefit portals

Avoid:

- Programs charging upfront fees

- “Guaranteed approval” claims

- Unverified social media ads

Housing affordability challenges have pushed governments to expand assistance programs.

Key trends include:

- Rising rents nationwide

- Declining first-time buyer participation

- Workforce housing shortages

- Increased political focus on affordability

Experts expect expanded funding—but tighter competition, making early awareness crucial.

Ans. First-time homebuyer grants are programs that provide free money to eligible buyers to help cover down payments and closing costs without requiring repayment.

Ans. Most grants do not need to be repaid as long as the buyer meets occupancy and program requirements.

Ans. Buyers may receive anywhere from $5,000 to $25,000 or more, depending on location and program eligibility.

Ans. Yes. Many programs allow incomes up to 120–140% of the area median income.

Ans. In many cases, yes. Buyers often stack state, local, nonprofit, and employer programs.

Ans. Most programs require a minimum credit score between 620 and 680.

Ans. Yes. All U.S. states offer some form of first-time homebuyer assistance.

Ans. Yes, as long as income documentation meets program guidelines.

Ans. Most grant programs require completion of a short HUD-approved education course.

Ans. Applications are typically processed through approved lenders or state and local housing agencies.

First-time homebuyer grants are not loopholes or gimmicks—they are intentional programs designed to help Americans build wealth through homeownership.

For many people, these grants mean:

- Buying years earlier

- Spending thousands less

- Avoiding unnecessary financial stress

If you’re planning to buy your first home, the most powerful step isn’t saving more money—it’s learning what free money you already qualify for.